By Sabrina Corlette and Rachel Schwab

January 16, 2024 Update: H.R. 824 was advanced by the U.S. House of Representatives’ Committee on Education & the Workforce in June 2023. More recently, advocates for the measure are pushing to attach the proposal to an upcoming appropriations bill as a “policy rider.”

On Tuesday, June 6, the U.S. House of Representatives’ Education & Workforce Committee will consider a bill, H.R. 824, that would encourage the proliferation of telehealth coverage as a standalone employee benefit. Proponents of this legislation—many of whom stand to profit from the sale of these products—argue that it would give employers and workers more affordable options. However, under the proposed legislation, standalone telehealth products would be almost entirely exempt from regulatory oversight, posing significant risks to consumers who could face deceptive marketing of these arrangements as a substitute for comprehensive coverage.

Background

The delivery of health care services via telehealth modalities expanded dramatically during the COVID-19 pandemic. Although rates of telehealth use have moderated somewhat since the height of the public health emergency (PHE), they remain well above pre-pandemic levels.

Federal and state policymakers encouraged the use of telehealth through several PHE-related policy changes. For example, early in the pandemic many workers were staying home and facing reductions in work hours, sometimes rendering them ineligible for health insurance through their employer. The Biden administration sought to help fill gaps in access to health services by issuing guidance temporarily suspending the application of group health plan rules to standalone telehealth benefits when offered to employees ineligible for the employer’s group health plan. This policy was only applicable during the PHE.

Ordinarily, any employer-sponsored plan covering medical services for employees and dependents is subject to Affordable Care Act (ACA) and other federal standards for group health plans. Thus, absent the PHE-related suspension of the rules, a standalone telehealth benefit would need to comply with, for example, mandates to cover preventive services without cost-sharing, the ban on annual dollar limits on benefits, mental health parity requirements, and the annual cap on enrollees’ out-of-pocket spending. However, H.R. 824 would extend and expand on the COVID-era policy by allowing employers to offer telehealth as an “excepted benefit” to all employees—not just those ineligible for the employer’s major medical plan.

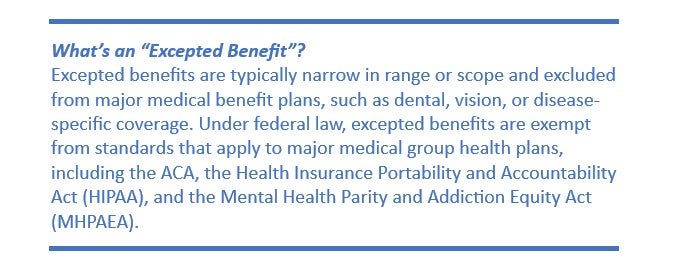

Excepted benefits can be attractive to employers because they are not subject to most federal standards that apply to group health insurance, including consumer protections under the ACA, HIPAA, and MHPAEA. Dental and vision insurance are among the most common types of excepted benefits, and many vendors notoriously provide insufficient coverage. Fixed indemnity insurance, another excepted benefit, is often marketed to consumers as comprehensive insurance coverage despite covering only a fraction of enrollees’ actual incurred costs.

Telehealth as an Excepted Benefit Would Reduce, Not Enhance, Quality Coverage

Nothing under federal law prevents employers from covering telehealth for employees, either by reimbursing brick-and-mortar providers for offering video and audio consultations or by contracting with telehealth vendors such as Teladoc. In fact, the vast majority of large firms (96%) and small firms (87%) currently cover some form of telehealth services. Designating telehealth coverage as an excepted benefit is thus unlikely to expand workers’ access to these services. Instead, the proposal poses several problems for workers and their families.

First, separating telehealth services from employees’ health benefits fractures care delivery and frustrates the coordination of care for patients, who will likely have to see a different provider than their usual source of care to access covered telehealth benefits. It could also subject enrollees to unexpected additional cost sharing, such as two deductibles, and cause confusion about what services are covered and by whom.

Second, designating telehealth coverage as an excepted benefit puts consumers at risk by encouraging the marketing of products that are exempt from critical federal protections. A telehealth insurer could charge a higher premium to someone with a pre-existing condition and refuse to cover certain treatments, or alternatively, the insurer could deny them coverage altogether. Excepted benefits are also exempt from mental health parity rules, can place annual or lifetime caps on benefits, and can impose cost sharing for preventive services, which may deter enrollees from getting the care that they need.

Third, excepted benefits have a troubled history, with vendors often deceptively marketing these products as an alternative to comprehensive health insurance. Brokers often package excepted benefit products together, so that they appear on the surface like a comprehensive policy, without clearly communicating that these arrangements do not comply with key consumer protections and leave enrollees at significant financial risk.

Fourth, a standalone telehealth benefit that an employee can choose in lieu of a major medical plan could disproportionately harm lower income workers. These workers may be encouraged to enroll in the telehealth benefit, potentially packaged with another excepted benefit such as a fixed indemnity policy, as an affordable alternative to their employer’s major medical plan. But workers may not realize that these products are not subject to the same consumer protections as the comprehensive group plan and do not provide real financial protection if they get sick or injured.

Conclusion

Expanded access to telehealth services has been a boon for patients, particularly those living in rural areas and those who lack transportation options or flexibility at work. Employers, to their credit, embraced telehealth during the pandemic and haven’t looked back. A whopping 76% of employers with 50 or more employees predict that the use of telehealth in their health plans will either stay the same or increase, and a substantial majority of both large and small firms believe that telehealth will be very or somewhat important to providing enrollees with access to a wide range of health care services, particularly for behavioral health.

Thus, while H.R. 824 is touted as expanding telehealth coverage, its main effect would instead be to silo medical services delivered through video and audio modalities from the rest of the care delivery system, increase the potential for scams and deceptive marketing, and expose workers and their dependents to health and financial risk by rolling back critical consumer protections.

4 Comments

Telehealth services are not appropriate to be designated as “excepted benefits”. Excepted benefits are insurance products that do not provide comprehensive major medical coverage, hence the reason these products are “excepted”. Excepted benefit insurance products are designed to be supplementary to major medical coverage and must not be marketed as major medical coverage,

MedPAC defines telehealth as “the exchange of medical information from one site to another by means of electronic communications to improve a patient’s clinical health status”. Telehealth services are not payers of insurance benefits of any kind. Telehealth services are in fact a “cost” that is paid for by major medical insurance coverage. Telehealth is not an insurance product and so should not be an “excepted benefit”.

Some lawmakers still favor the Spartan concept. The weak do not deserve to be taken care by the strong.

If congress would pass this bill some weaklings like Stephen Hawkings may not shed light on some of the lights , wonders and the unknown and hidden life in the universe.

Those who have less means and income need the help of those who have more to make the country stronger. This has been the spirit that made the USA a strong nation .

Integrating telehealth as an essential part of comprehensive coverage improves accessibility, convenience, and cost-effectiveness in healthcare delivery. Let’s embrace this paradigm shift and leverage telehealth to enhance patient care.